Cambria Swanson

Living Abroad as an American Retiree

Over 5.5 million Americans now live abroad, and that number continues to grow each year. For many retirees, life overseas means lower living costs, slower pace, and greater cultural richness.

However, one of the biggest concerns for soon-to-be expats remains clear:

How will healthcare and Medicare coverage work once I leave the U.S.?

A Personal Look: What Expats Are Saying

Many retirees who relocate to countries such as Spain, Portugal, or Costa Rica describe their new healthcare experiences as efficient, affordable, and surprisingly high-quality.

For example, one retiree in Madrid said:

“I was nervous at first about giving up Medicare coverage, but after visiting a private clinic here, I realized the quality matched what I had in the U.S. — at a fraction of the cost.”

Their stories remind us that understanding both Medicare options and international healthcare alternatives is crucial before moving abroad.

What is Medicare?

Medicare iWhat Is Medicare? (2025 Overview)

Medicare provides health coverage primarily for people aged 65 or older and certain younger individuals with disabilities, ALS, or End-Stage Renal Disease.

While Medicare is a powerful program within the U.S., it does not extend full coverage overseas — a critical factor for expats to understand.

Should You Keep Medicare Coverage Abroad as a U.S. Expat?

Keeping Medicare can make sense for certain expats — especially if you plan to return to the U.S. or want to avoid penalties. However, if you plan to live permanently abroad, you might find that maintaining Medicare is not worth the cost.

Reasons to Keep Medicare Abroad

- Avoid late-enrollment penalties when returning to the U.S.

- Maintain eligibility for Part A (premium-free).

- Peace of mind if you frequently travel between the U.S. and another country.

Reasons to Cancel Medicare Abroad

You have no intention of returning to the U.S.

You have local or international health coverage that provides full care in your new country.

You want to save on Part B premiums ($175/month in 2025).

Costs and Penalties (2025 Update)

Medicare costs and penalties can add up quickly.

- Part B Premium (2025): ~$175/month.

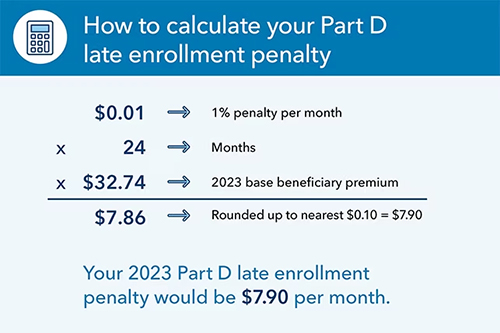

- Part D Penalty: 1% per month for every month you go without coverage.

- Part B Penalty: 10% for every year you miss enrollment.

For more information on these penalties, visit Kaiser Permanente’s Medicare Penalty Guide.

Late enrollment penalties | Kaiser Permanente. (n.d.). Kaiser Permanente. https://healthy.kaiserpermanente.org/washington/shop-plans/ready-for-medicare/late-enrollment-penalties

This image is a perfect example of the significant impact that a penalty can have on the cost of Medicare. A 1% penalty per month for Part D Medicare can incur an increase in costs of almost $100. This cost quickly adds up and is one that can easily be avoided.

Part A is slightly different in the way that it does not usually require a premium. This coverage is free. It is recommended that you keep this Medicare plan. Especially if you are planning on moving back to the U.S., maintaining this plan will avoid gaps in coverage. There is a premium version of Part A, which can be very costly. Disenrolling in Part A requires paying back the benefits back to the Social Security Administration. If a citizen cancels their plan and moves back to the United States, they run the risk of living months without any health insurance. In this instance, it is best to maintain coverage with at least the premium-free Part A to avoid future penalties. It does not make sense to maintain Medicare coverage if the American does not foresee moving back to the United States.

Healthcare Systems Abroad: Spain as an Example

Spain is one of the most popular destinations for U.S. expats on Medicare to retire. The country offers both public and private healthcare systems that rank among the best in the world.

Public Healthcare in Spain

- Available to legal residents who contribute to the Spanish Social Security system.

- Covers GP visits, hospital stays, prescriptions, and emergency care.

- Highly rated for quality and accessibility.

Private Healthcare Options

- Private insurance plans such as Cigna Global, Sanitas, Mapfre, AXA Health, and ASISA offer quick appointments and English-speaking doctors.

- Annual premiums are often less than a few months of U.S. Medicare costs.

Dual Coverage

Many Americans abroad maintain both systems — using public healthcare for regular visits and private insurance for specialized care.

Learn more about Spain’s healthcare system on the U.S. Embassy in Madrid’s Medical Assistance page.

Practical Tips for U.S. Expats Managing Medicare Abroad

- Keep Part A if it’s free — it won’t hurt to retain it.

- Cancel Part B if you’re sure you won’t return to the U.S., but weigh the risk of re-enrollment penalties.

- Compare international insurance providers to find plans that cover multiple countries.

- Budget carefully — include exchange rates, premiums, and emergency coverage.

- Keep records of all your U.S. Medicare communications and Social Security forms.

Additional Resources for U.S. Expats and Medicare Abroad

- Medicare and You 2025 Handbook (Official U.S. Guide)

- Social Security Administration – International Programs

- Centers for Medicare & Medicaid Services – Policy Updates

Share Your Experience

Have you navigated healthcare abroad as a U.S. expat?

Share your story in the comments — your experience can help others prepare for retirement overseas.

If you’re considering a move abroad or currently living overseas, schedule a consultation with Cross Border Wealth Advisors.

We specialize in financial and tax planning for Americans abroad, including strategies for Medicare abroad, global healthcare, and retirement planning.